Strait Theatre

And The Coordinated Energy Realignment

This was not a war. It was a restructuring exercise carried out under the cover of one. The U.S. has done this before — manufacture or accelerate a crisis, let the disruption clear the board, then move in as the stable expensive alternative. Gulf of Tonkin. Iraqi WMDs , Ukraine. The pattern isn’t new. What’s new is the scale of the commercial infrastructure that was already waiting to absorb the outcome.

Energy infrastructure was repositioned, trade corridors were reset, proxy liabilities were burned off, market share was redistributed, and the region’s financial architecture was quietly re-engineered while the public drowned in spectacle. The violence supplied the legal, political, and insurance rationale for outcomes already mapped in filings, planning documents, and funding commitments years before the first fake missile was launched.

They called it a war. It was a business deal and they were all in on it.

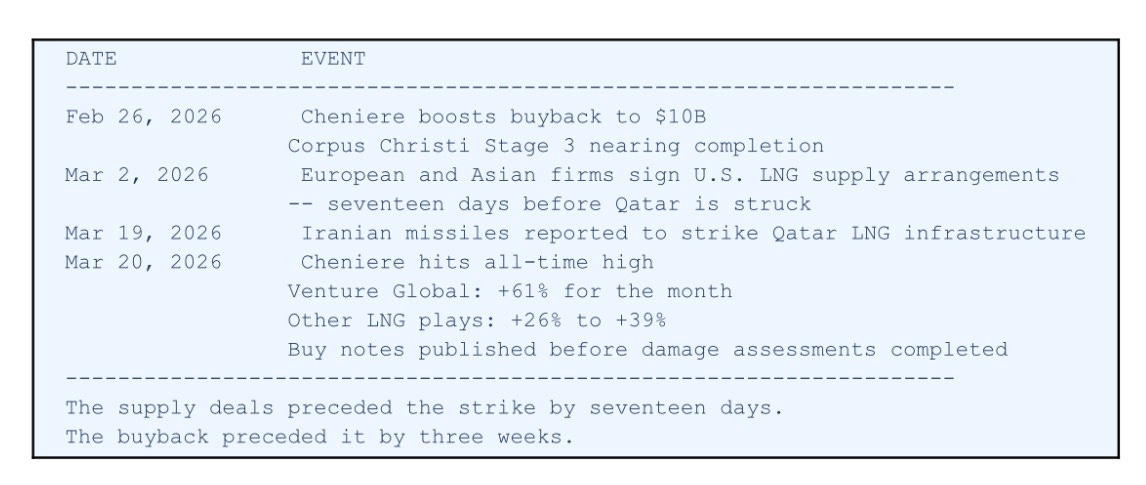

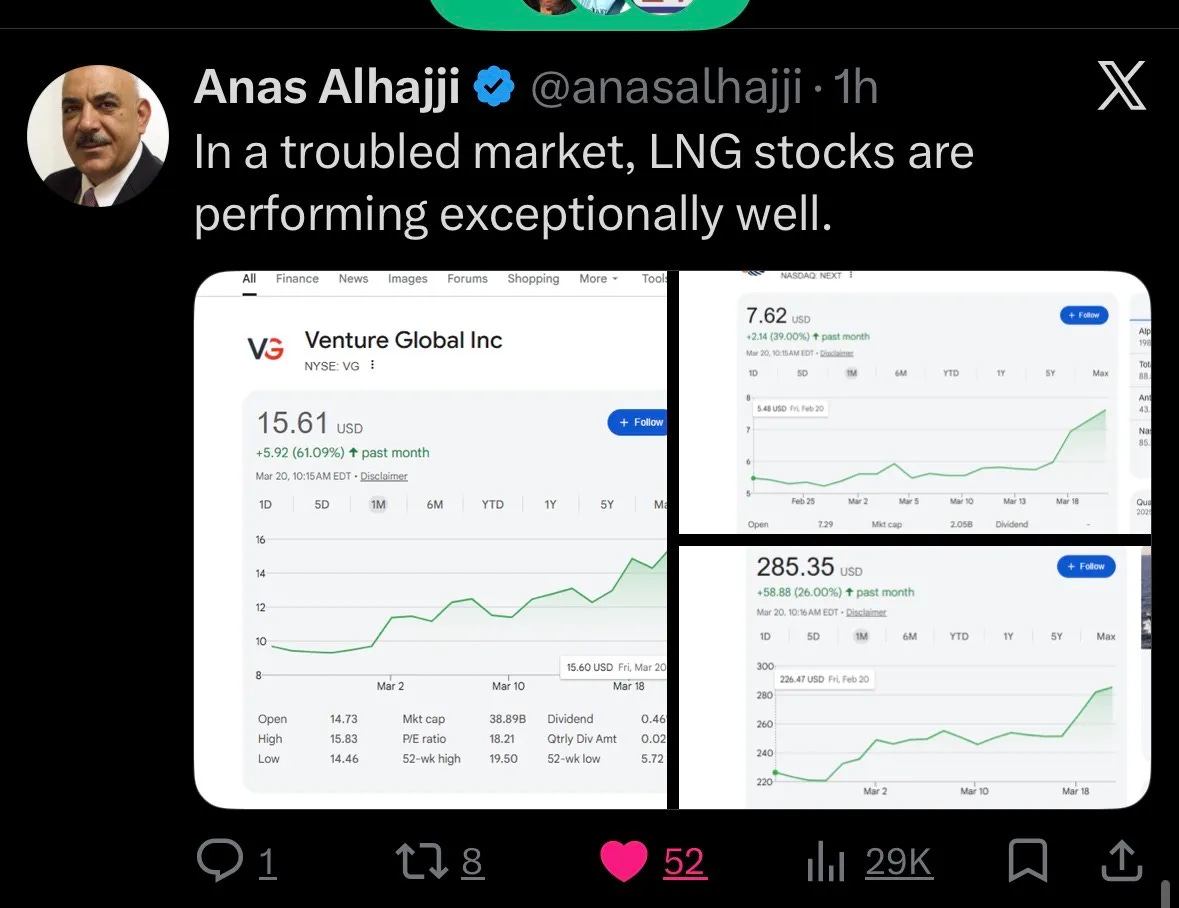

On March 19, 2026, Iranian missiles were reported to have struck Qatar’s LNG infrastructure at Ras Laffan. By the following morning, Cheniere Energy had hit a new 52-week high, touching $260.49 intraday before closing at $261.30. Venture Global was up sixty-one percent for the month. Bank of America raised its price target to $322. Buy notes were circulating before the damage assessments were complete.

Three weeks earlier, on March 2, Venture Global and Trafigura executed a binding LNG supply agreement filed directly with the SEC — approximately 0.5 million tonnes per annum of U.S.-sourced LNG commencing in 2026. European and Asian buyers had already signed forward supply arrangements. The gap those contracts were designed to fill opened seventeen days later.

On March 20 — LNG was up, fertilizer exposure up, chemical names up, U.S. firms absorbing rerouted demand — was a position being realized, not a reaction to surprise. Positioning of that precision requires knowing the direction.

Seems to happen a lot with these “wars”

Make no mistake, Washington knew exactly what it was doing. The Biden LNG pause was always temporary scaffolding — a regulatory hold that kept the export queue frozen while the infrastructure buildout continued underneath it. The moment it became useful to lift it, it was lifted. Day one of Trump’s second term, the DOE ended the pause and called it “returning to regular order.” Regular order was the plan all along.

The numbers tell you why. North American LNG export capacity was already on track to nearly triple by 2029 — from 11.4 to 28.7 billion cubic feet per day — accounting for over half of all projected global additions. That buildout didn’t start in response to the conflict. It was already underway. The conflict made it legible as strategy rather than opportunism.

Meanwhile Bloomberg ran the headline openly: American LNG billionaires positioned to profit from war with Iran. Venture Global’s founders were photographed at Plaquemines under construction in May 2024 — months before any escalation. The capital was already in the ground.

THE BUILDOUT

While war framing dominated coverage, the Gulf was executing one of the largest coordinated energy expansion cycles in decades — roughly eighty billion dollars in committed capital, publicly filed, with phases scheduled years in advance across five countries.

Qatar alone was targeting an expansion from 77 to 142 million tonnes per annum by 2030, with contracts signed and equipment ordered years before any of this began. The region was already mid-execution on a generational infrastructure overhaul with permits in place, budgets allocated, and contractors mobilized on a fixed timetable.

A force majeure event in a zone already mid-transition provides exactly the cover needed to accelerate a phase-out, absorb a redevelopment cost, and collect insurance on assets already scheduled for retirement.

Do you really think this level of market precision — supply deals signed seventeen days before a strike, buybacks authorized three weeks prior, price targets raised before damage assessments were in — is random timing?

THE DEMOLITION SCHEDULE

The overlap between reported strike locations and pre-filed redevelopment plans holds across every major site in this conflict cycle. These are not exactly buried footnotes.

Saudi Arabia’s old airport got “struck by Iranian missiles.” Saudi Arabia’s new airport — Jeddah Terminal 1, opened 2024 — has a floor-to-ceiling coral aquarium in the arrivals hall, cathedral ceilings with Islamic geometric latticework lit in blue, and a check-in hall that looks like a luxury hotel lobby.

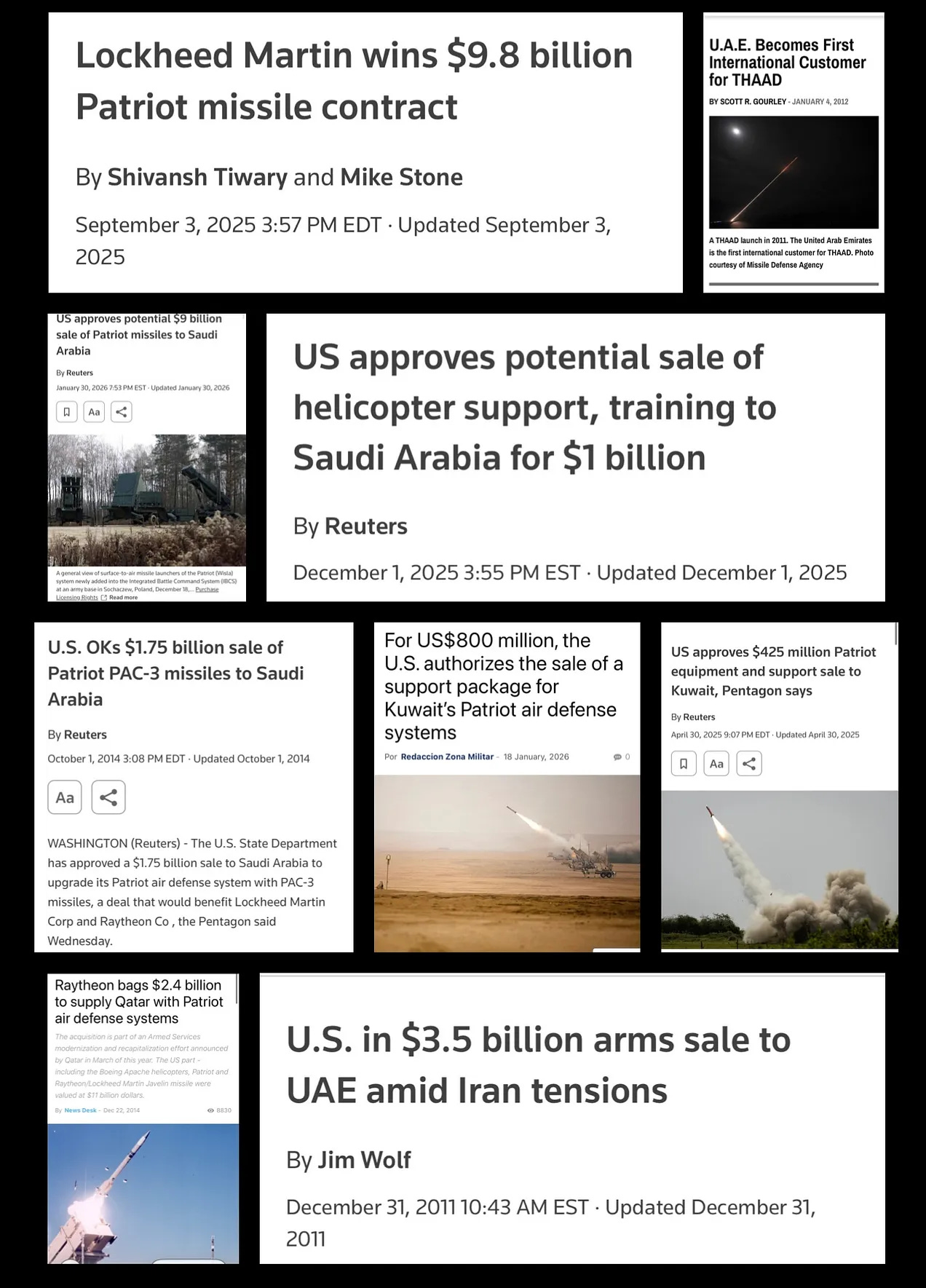

The country that bought $9 billion in Patriot missiles in January 2026 and $1.75 billion in PAC-3 upgrades before that, whose air defenses apparently couldn’t stop Iranian ballistic missiles from hitting its airports, just happened to have a gleaming replacement terminal already open and operational.

UAE

The Jebel Ali industrial zone sits adjacent to a published masterplan for Palm Jebel Ali: 13.4 square kilometres of luxury waterfront development, twice the size of Palm Jumeirah, adding 110 kilometres of new coastline to Dubai.

Kuwait

Kuwait’s old airport was struck. Tragic. The new one cost $4.3 billion, was already under construction, and wasn’t touched. Funny how that works.

Israel

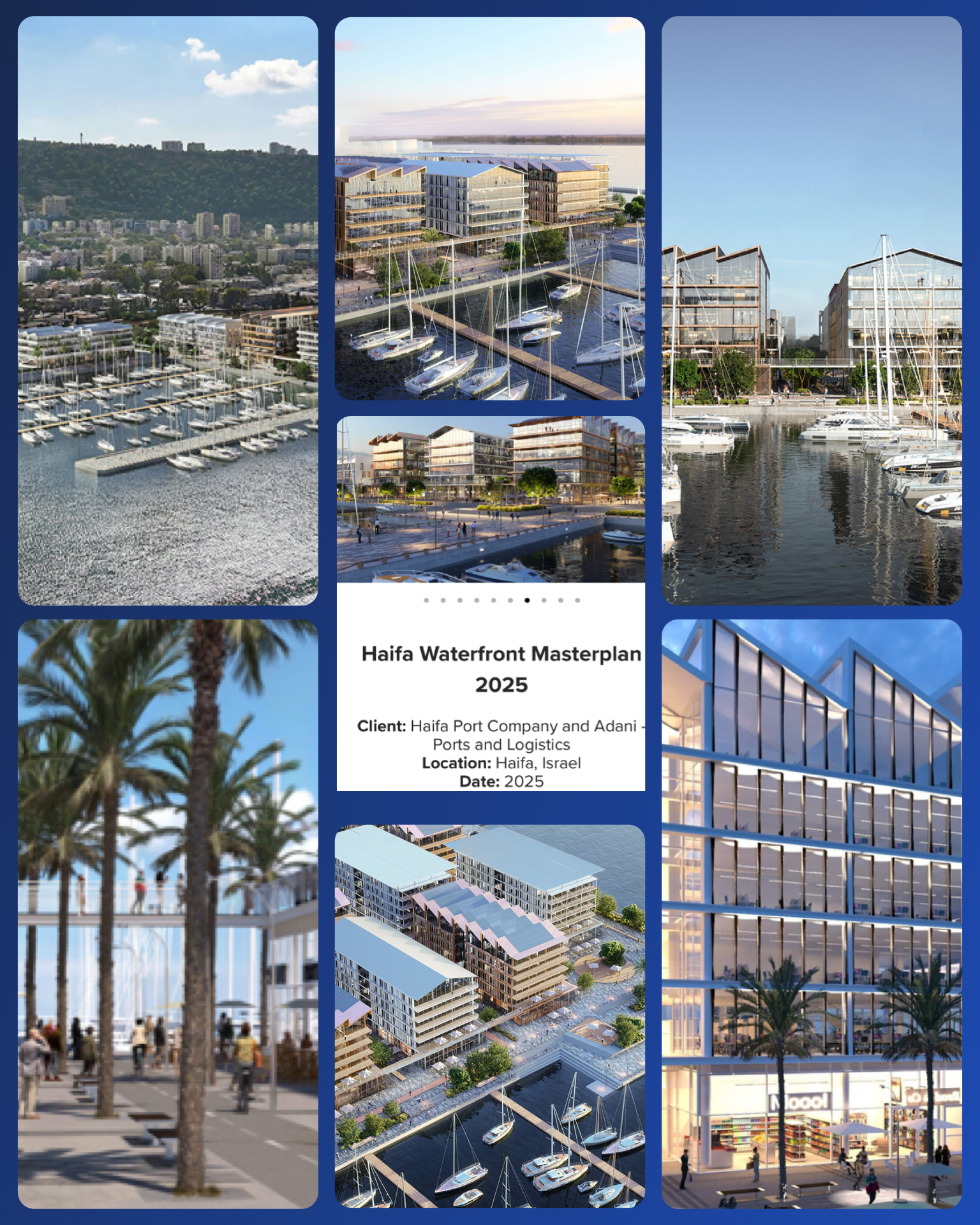

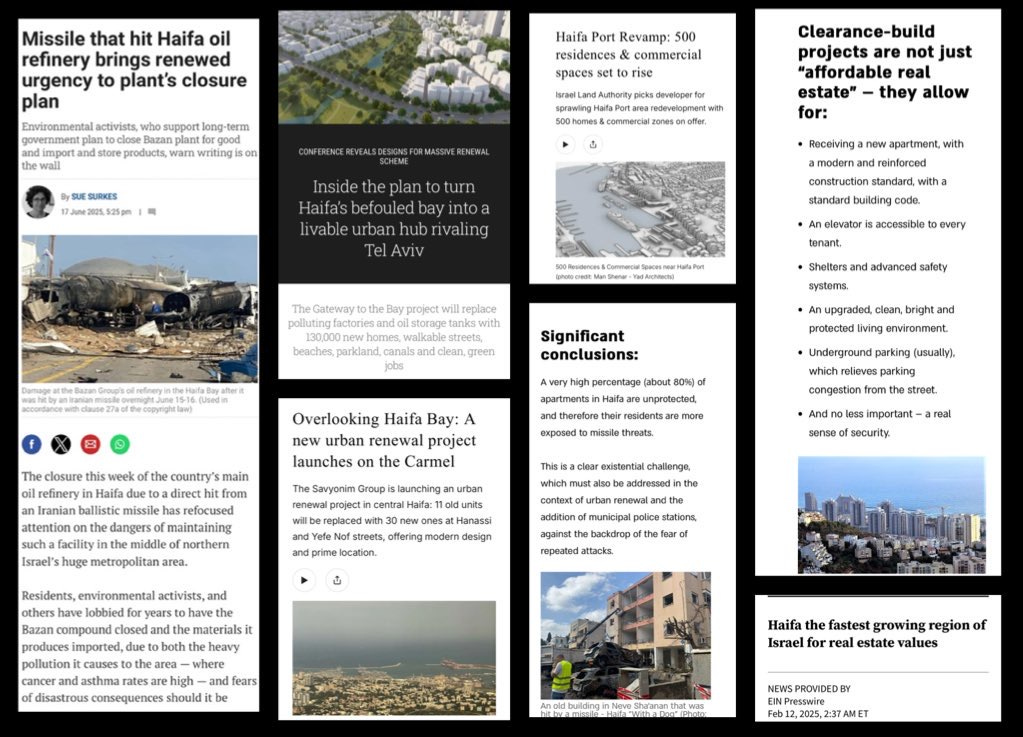

The Haifa story is worth slowing down on — the narrative is transparent and the people paid to repeat it are still working overtime. Bazan, Israel’s primary oil refinery, was struck in June 2025 — allegedly killing three workers — and targeted again in this cycle. What they don’t ever mention is that the Israeli government voted in 2022 to relocate it entirely by 2030, citing urban environmental risk. A McKinsey report had already estimated the relocation cost at $5.2 billion while explicitly flagging the site’s value as prime Haifa waterfront real estate. What was notably untouched in both strikes: the adjacent Haifa Port, acquired by Adani for $1.15 billion and positioned as a key node on a Europe-to-Gulf trade corridor. The facility already scheduled for demolition absorbed the damage. The recently acquired strategic asset did not.

The Dimona episode follows the same logic. On March 21–22, Iranian missiles were reported striking Dimona. The IAEA immediately confirmed zero damage to the nuclear site and zero radiation release. The actual impact zone was a residential block approximately twelve kilometers from the reactor — in a neighborhood the Casiopea Group had already flagged for urban renewal and demolition, a project stalled for years by resident opposition and permit disputes. A declared security incident fast-tracks government-funded demolition in ways that routine planning processes cannot

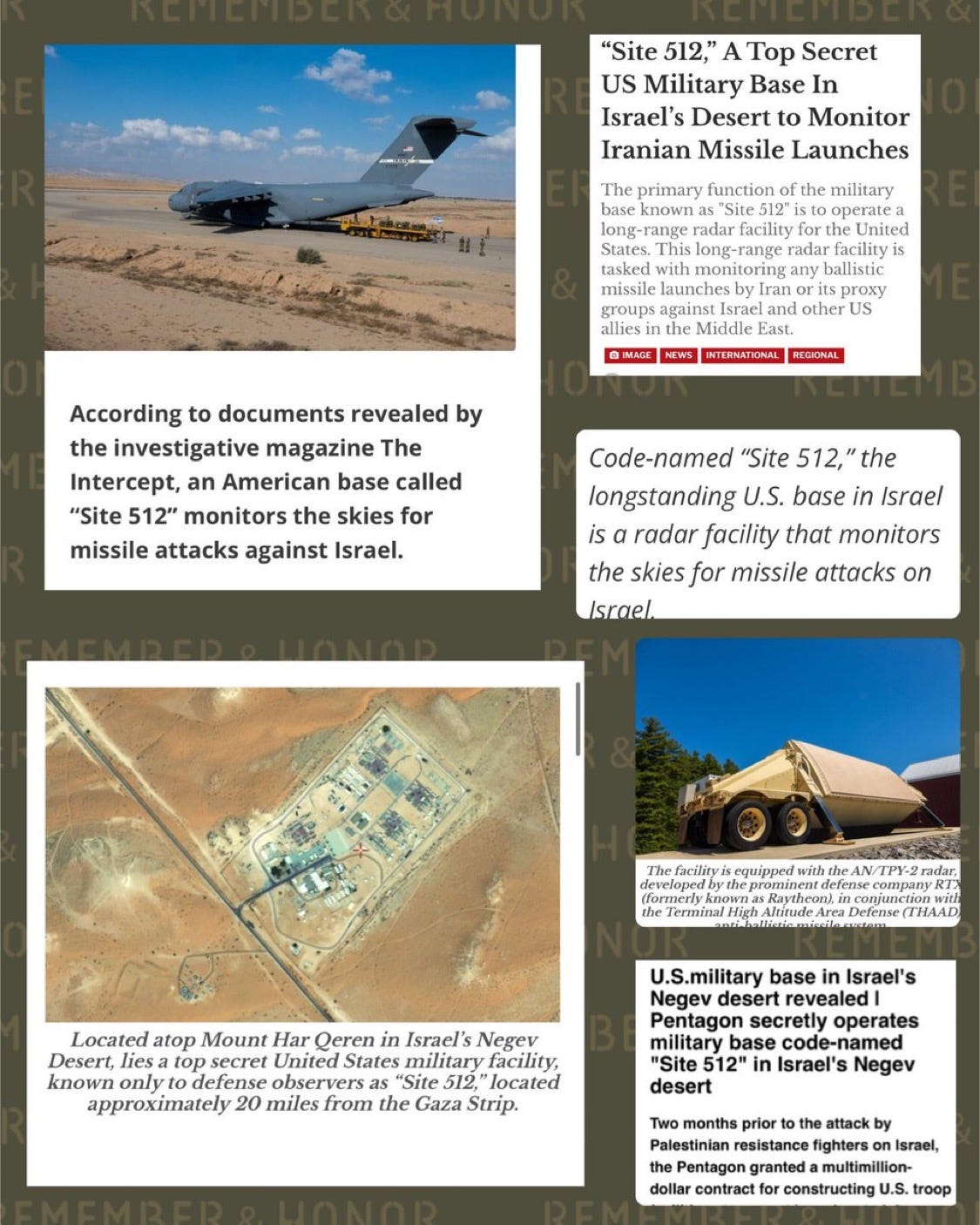

Also relevant: Site 512 — the U.S. AN/TPY-2 radar installation in the Negev, directly linked to THAAD — provides real-time trajectory data on Iranian missile launches. If a genuine Iranian ballistic missile struck within twelve kilometers of Dimona, the United States had full tracking data from launch to impact. That data has not been released or formally requested by any major outlet.

THE ONLY AIRCRAFT WE ACTUALLY TRACKED

Throughout the entire period that strikes were being reported across the Gulf, Iraq, and Iran, open-source flight tracking showed one consistent pattern: the only military air presence visible with regularity over the strike corridors was American.

U.S. Air Force tankers. ISR platforms. Support aircraft operating over Israel and threading into Jordanian airspace, present at operational density in the corridors bracketing every reported strike zone. The density and geographic concentration were consistent with an air force actively coordinating sustained operations — refueling, directing, enabling — not a force that happened to be in the vicinity. This pattern was present before, during, and after every reported strike event in this cycle.

If Iranian ballistic missiles were genuinely operating at the reported scale and frequency, the open-source air picture would reflect Iranian launch signatures, intercept attempts, and the kind of defensive scramble that leaves a traceable record across multiple tracking platforms.

ROAD TO NOWWHERE

The Iraq Development Road is a $17 billion infrastructure project formally inaugurated by Prime Minister al-Sudani on December 5, 2025, with 63 kilometers of road already laid from Grand Faw Port toward Khor Al Zubair. A 1,200-kilometer road and rail corridor connecting Basra to the Turkish border, bypassing the Strait of Hormuz entirely and routing through no U.S.-aligned financial chokepoint. Grand Faw Port alone was projected to handle 55 million tonnes of cargo annually — generating an estimated $4 billion per year in transit revenue for Iraq. Significant Chinese engineering involvement throughout. Sitting directly across BRI strategic geography.

That is the Development Road mapped onto a strike list, node by node, before the corridor could become operationally viable. Iraq’s government had explicitly decided to sit out the conflict. Iraq was the geography being managed. The corridor that would have given Iraq, Iran, and China structural leverage over Gulf trade routing has been set back by years at the precise moment it was becoming real.

Do you really think Iran would take hits on Chinese investment corridors and trade routes in ways that benefit competing flows ?

IRAN’S CALCULATION, AND THE PROXY BALANCE SHEET

Iran has spent years repairing ties with Saudi Arabia, keeping channels open with the UAE, and positioning Qatar as a mediator. The 2023 Saudi-Iran normalization brokered through Beijing was the most significant Iranian diplomatic win in a decade. Reuters reported that after strikes on Iran’s South Pars and Asaluyeh facilities, Tehran issued evacuation warnings to Gulf energy sites before further strikes were reported — warnings before strikes being the behavior of a state managing escalation calibration, not one trying to permanently sever a relationship.

Iran has never treated détente as immunity. The logic has always been transactional: pressure without rupture, as long as Gulf states remain commercially useful and are not actively facilitating attacks on Iranian territory. Tehran warned Gulf energy sites before striking them.

You don’t warn targets you’re trying to destroy.

As for the proxy theatre—these groups have outlived their utility and are now a liability — which is kind of bullshit when you consider how these groups were created.

Hezbollah, the Houthis, the Iraqi militia constellation — were the single largest structural obstacle to its sanctions relief and financial reintegration. Not only in Washington, but in European capitals, in Gulf states Iran had been quietly normalizing relations with, and in every international financial institution that Iran’s modernization agenda required access to. Proxy entanglement is designated risk. It cannot be hedged or cannot be disclosed away. It kills deals in risk committees regardless of the commercial case underneath.

Engineered Resistance:

The constant bombardment of war imagery surrounding the Israeli-Palestinian conflict has transformed real suffering into ritualized spectacle. Repetition of destruction, media-driven confrontations, and manufactured threats has dulled public perception. The effect is deliberate. These narratives sustain geopolitical agendas while numbing the audience to…

And here is the part worth sitting with. The Houthis are supposedly operating in Yemen — one of the poorest countries on earth, under active Saudi bombardment for a decade, with no meaningful air force, no blue-water naval capacity, no satellite targeting infrastructure, and no logistics chain capable of sustaining precision strikes across multiple theatres. Yemen cannot project force into the Red Sea at scale and sustain it- yet they’re referred to as a proper military? Ask yourself why?

Remove the proxy liability from Iran’s balance sheet — particularly if it is removed in a conflict Iran can credibly frame as imposed rather than chosen — and the investment case changes entirely. Sanctions relief discussions were already circulating before this escalation cycle began. The nuclear framework conversations never fully died. Iran’s undeveloped hydrocarbon reserves are among the largest on earth. The conversation in Zurich, Singapore, and Dubai about Iranian energy asset exposure moves from theoretical to executable.

Do you really think Iran would do this to the Gulf states it spent two years normalizing with — and that those states would not respond with anything beyond carefully worded statements, if this were a genuine uncoordinated attack?

“PREPAREDNESS”/FINANCIAL TIMELINE RECAP

The US has been planning this for a long time. . Integrating U.S. and Israeli air defense networks, aligning command structures, running live-fire drills at that scale — that’s years of planning, budgeting, and logistical groundwork. They weren’t responding to a threat environment as much as they were building one.

Feb 26, 2026

Cheniere Energy announces $10B share buyback authorization through 2030. Corpus Christi Stage 3 nearing completion. Q4 2025 EPS: $10.68 — beat analyst consensus of $3.90 by $6.78.

Feb 26, 2026

Venture Global executes 20-year LNG SPA with Hanwha Aerospace — 1.5 million tonnes per annum from 2030.

Mar 2, 2026

Venture Global and Trafigura execute binding LNG supply agreement — filed with the SEC. 0.5 MTPA commencing 2026. Seventeen days before Qatar’s infrastructure is struck.

Mar 13, 2026

Venture Global CP2 raises $8.6B for Phase 2 — SEC 8-K filed. Total CP2 funding: $20.7B. One of the largest U.S. energy project financings on record.

Mar 18, 2026

Cheniere hits intraday all-time high of $267.24 as Hormuz closure drives natural gas up 5.59% to $3.20/MMBtu. Thailand expands LNG order from 1M to 1.3M tonnes.

Mar 19, 2026

Iranian missiles reported to strike Ras Laffan LNG complex. Per QatarEnergy CEO: 17% of Qatar’s LNG capacity offline, three to five years to repair. North Field expansion work halted…. So the US can charge 20 times th

Mar 20, 2026

Cheniere hits new 52-week high at $261.30. Venture Global +61% for the month. BofA raises price target to $322. Buy notes published before damage assessments completed.

It should also be said that the Gulf states benefit. Saudi Aramco holds equity stakes in U.S. refining and downstream infrastructure. ADIA, PIF, QIA — all deeply positioned in Western energy and finance. When Western energy markets win, they win twice: on their own exports, and on their portfolios. The conflict didn’t hurt them. It paid.

WHAT THE RECORD SHOWS

Nothing here requires much interpretation because the sequence is already on the record, and what it shows is not a set of isolated events but parts of the same larger realignment. The plans were in place before the strikes, the financial positioning came before the supposed trigger, and the only consistent military air presence over those corridors was American. What followed was a chain of outcomes that fit together with remarkable precision: Iran’s proxy layer was removed, Iraq’s competing route was delayed, Gulf redevelopment advanced under wartime cover, U.S. LNG picked up market share, and Iran’s path toward reintegration was opened.

It also fits a wider move to contain China’s regional leverage. A functioning Iraq-Iran corridor would have given Beijing more room to move energy, goods, and capital through partners operating outside U.S.-controlled Gulf routing. That corridor is now set back by years. The old bottlenecks stay in place, Gulf flows remain tied to American security architecture, and Washington keeps its hand on the map where it matters most.

Syria is the next obvious piece. Once the surrounding routes, proxies, and pressure points have been reordered, the remaining question is which territory gets folded into the next phase of corridor control, reconstruction contracts, and regional discipline. The answer has been visible for some time.

Mark my words: they’ll create some kind of joint patrol mechanism — a straits monitoring unit, a maritime security coalition, something with a neutral-sounding name. Officially it’ll be there to keep the shipping lanes open. Everyone will know what it’s actually for. Permanent military infrastructure in the Strait of Hormuz, dressed up as a traffic cop. The surveillance and force projection implications write themselves.

The financial system has a long and documented history of wars that happen to benefit the people positioned to benefit from them — and those people are rarely the ones doing the dying. The United States just manufactured a conflict in a region it has destabilized for decades to permanently damage the only credible competitor to its LNG dominance, and to lock in the contracts that will fund the next generation of export terminals. Qatar’s thirty-year reliability record is gone.. at least for a little while. The states and firms that went looking for a way out of American supply coercion are now left holding disruption notices, suspended deliveries, and contracts that turned to paper the moment the pressure campaign reached its endpoint. That is how power functions in this system: options are narrowed, dependence is rebuilt, and then the outcome is presented to the public as an unfortunate crisis nobody could have foreseen. The more dangerous part is how many people still absorb that story through a media environment that lies as routinely as it breathes, asking no questions about timing, beneficiaries, or who stood to gain from the breakdown. So the issue is no longer whether any of this is ugly enough to deserve outrage. The issue is how to protect your money, your assets, and your future in a world managed by people who do business through coercion, engineered shocks, and narrative fraud.

Excellent analysis. And you're the only one talking about this angle (which becomes more plausible with every article).

What better way to achieve your goals of quickly dismantling current infrastructure on a large scale than with a cover story like this one. You bypass regulatory hurdles, opposition, and anything else that might impede your progress - no questions asked. It all falls perfectly under the umbrella of “War is hell, things get blown up”, and nothing more needs to be said.

In a climate of severe reality-distortion, if we are being treated to a montage of real controlled demolitions, interspersed with dramatic AI war footage simulations, who could even tell?

It seems propaganda has achieved new heights of sophistication, where we've entered into an era of grand narratives; multi-layered, challenging to detect, challenging to analyse, and becoming increasingly difficult to discern from actual reality. At this level, believing in anything with certainty becomes impossible.

Brilliantly researched and analysed.

Can we republish a small part of this in The Light paper next month?

https://thelightpaper.co.uk/

Peace.